Connect with a Lima One expert today!

If you’d like to know more about this topic or see how it applies to your project, let’s talk.

Understanding DSCR and Non-Owner-Occupied Loans

In the world of real estate investment, the search for financial solutions that solve the intricacies of non-owner-occupied properties often leads investors to explore specialized loan programs.

DSCR (Debt Service Coverage Ratio) loan programs in particular and non-owner-occupied investment property loans in general can facilitate real estate investment. DSCR loans are specifically designed to cater to the unique challenges and opportunities associated with non-owner-occupied real estate.

By explaining the concept of DSCR loans to exploring the pivotal role these loans play in real estate investing, this blog will help investors understand how these financial tools can open doors to new possibilities of property investment.

Introduction to Non-Owner-Occupied Loans

Investing in real estate can be a lucrative venture, offering both financial stability and growth opportunities. For investors looking to expand their portfolios, non-owner-occupied loans can be crucial tools in real estate investing.

Understanding How Non-Owner-Occupied Loans Work

Non-owner-occupied loans, also known as investment property loans, differ from traditional mortgages in that they are specifically designed to finance properties an owner doesn’t live in. These loans give investors the ability to finance properties intended for rental or investment purposes.

Unlike owner-occupied loans, which cater to personal residences, non-owner-occupied loans are tailored to meet the specific needs of investors looking to capitalize on rental income or capital appreciation. This flexibility opens doors to a diverse range of investment strategies and property types.

Non-owner-occupied loans can be made to individuals or to LLCs. The ability to lend to LLCs through business purpose loans allows more flexible options, including streamlined underwriting and documentation.

Non-Owner-Occupied Loan Requirements

Generally, rates on non-owner-occupied loans tend to be higher than those for owner-occupied homes. Lenders generally view investment properties as riskier ventures, leading to slightly elevated interest rates.

Creditworthiness is paramount for lenders evaluating non-owner-occupied loan applications. Investors with a strong credit history and financial stability are more likely to secure favorable loan terms.

The good news is that business-purpose lenders like Lima One will consider 1099 income when determining creditworthiness, while owner-occupied loans often focus only on W2 income.

Investors should also be prepared to show the property's income-generating potential. This is measured through the DSCR calculation, which is explained below.

An Overview of DSCR Loans

DSCR helps lenders and investors measure the ability to pay debt from the cash flow generated from the income property. It’s much like debt-to-income ratio in residential real estate with one major difference:

- DTI percentage is based on personal income, while DSCR is based on the property’s income.

- DSCR loans are versatile and offer financing solutions for short and long-term rentals, single family rentals, a portfolio of SFR homes, and multifamily units.

So, what is DSCR?

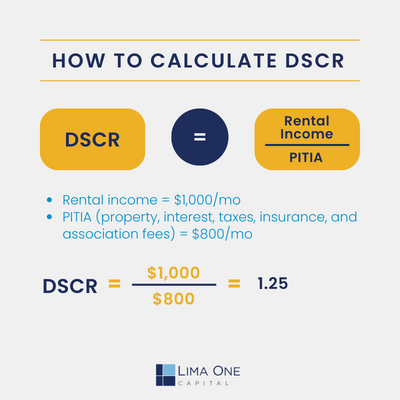

DSCR stands for Debt Service Coverage Ratio. It’s a calculation that compares your rental income on an investment property to the expenses of the investment. There are certain costs to consider when calculating DSCR: principal, interest on the real estate loan, taxes, insurance, and association fees.

Rental income is divided by the sum of the costs to create a DSCR value. A number above 1 indicates that a property cash flows.

Generally, lenders look for DSCR values of 1.2 or more, to make sure properties have surplus funds to address irregular costs like CapEx investments and vacancies.

It’s important to note that DSCR requirements may be different for long and short-term rental loans.

Lima One’s DSCR loans are a great financing option for both experienced and first-time real estate investors.

The great thing about DSCR loans is that investors don’t necessarily need a lot of capital to start building real estate wealth.

The Intersection of DSCR Loan Program and Non-Owner-Occupied Loans

Understanding the relationship between non-owner-occupied loans and DSCR loans is crucial for savvy investors. Knowing the difference can help investors scale their business and add to their portfolio – ultimately creating more revenue.

For real estate investors who have established properties that are already generating positive cash flow, DSCR loans are a great tool for leveraging equity, scaling their business, and taking their real estate investment property portfolios to the next level.

And Lima One is the private lender you want to work with. Our diverse product suite is designed to allow us to cater to the individualized needs of our investors, and our experienced lenders will help you find the right financing based on your investment strategies.

Contact us today to discuss your next deal, or if you have a deal in hand, accelerate the process by applying now.

Subscribe for More Insights

Get the latest industry news & Lima One updates.